One of the reasons economic and financial systems are so fascinating is that they are complex. Of course this is also one of the reasons why they are so frustrating. A current fascination/frustration of mine is inflation and its transmission through the economy. I readily admit that it is a complex beast whose workings I don't fully understand, so consider the following thoughts an exploration.

There has been much talk lately about how a period of modest inflation will benefit the economy. This makes sense to me given the broadest definition of inflation. In an economy overburdened by debt, decreasing the real value of those debts via inflation will improve the debt load on the borrower.

Unfortunately, I don't understand how we get broad inflation, by which I mean simultaneous consumer price inflation and wage inflation. It makes sense to me that the Fed, by lowering interest rates, can push asset prices higher and provide corporations and borrowers an incentive to refinance debt thereby improving balance sheets and increasing cash flows. It also makes sense to me how this could put upward pressure on consumer prices in multiple ways including marginally lowering the value of the dollar and increasing costs for imported goods. And of course lower interest rates make saving less attractive and consumption (theoretically) more attractive. In our current economic environment there is also growing pressure on rents which make up a large portion of consumer price inflation measures. This, however, seems more to do with an increase of rental demand after a housing bust more than anything else. I also understand that these are only a subset of the numerous other mechanisms through which lower interest rates support the general price level.

What I really don't get is how increased inflation supports wage inflation as directly, specifically employment income. Income from investment, sure, that makes sense. With lower interest rates supporting higher asset prices and refinancing activity decreasing debt finance costs, the mechanism here seems pretty direct. But how does this translate to support for income earners whose primary income derives from labor? That seems far less straight forward.

Given their improved balance sheets, employers will likely have increased room to hire if demand picks up. But to the extent that demand is dependent on consumption (and it is significantly dependent on it in America today), it seems we have a chicken or the egg type problem. Until income grows, demand is unlikely to grow. But until demand grows, income is unlikely to grow. Will consumption really be meaningfully stimulated for people with low savings and debts that were too large to begin with? Should it be? And with a relatively high unemployment rate, average wages per employee are not going to see significant pressure to rise either (though clearly, growing employment increases aggregate income even at a constant wage level).

I don't know how to quantify this, but my sense is that the median income derived from capital across all people earning an income from labor is small. Another way of saying that is that I think most people in the labor force don't have significant investment income. So I'm guessing that income from capital will not be a huge stimulus for the large majority of the labor force. Perhaps aggregate income will increase inline with inflation; that is, total personal income in nominal terms will grow at or above the rate of general inflation. But will income derived solely from labor grow at that rate?

I'm curious about this because we've seen the best measure of the middle of the income distribution, real median household income, decline over the last couple of years. So are these folks falling behind in real terms because monetary policy has a less direct (or perhaps slower) impact on wages? That the median household income in the US declined by 6.2% from 2007 to 2010 suggests that they at least were falling behind up to that point. Will they catch up?

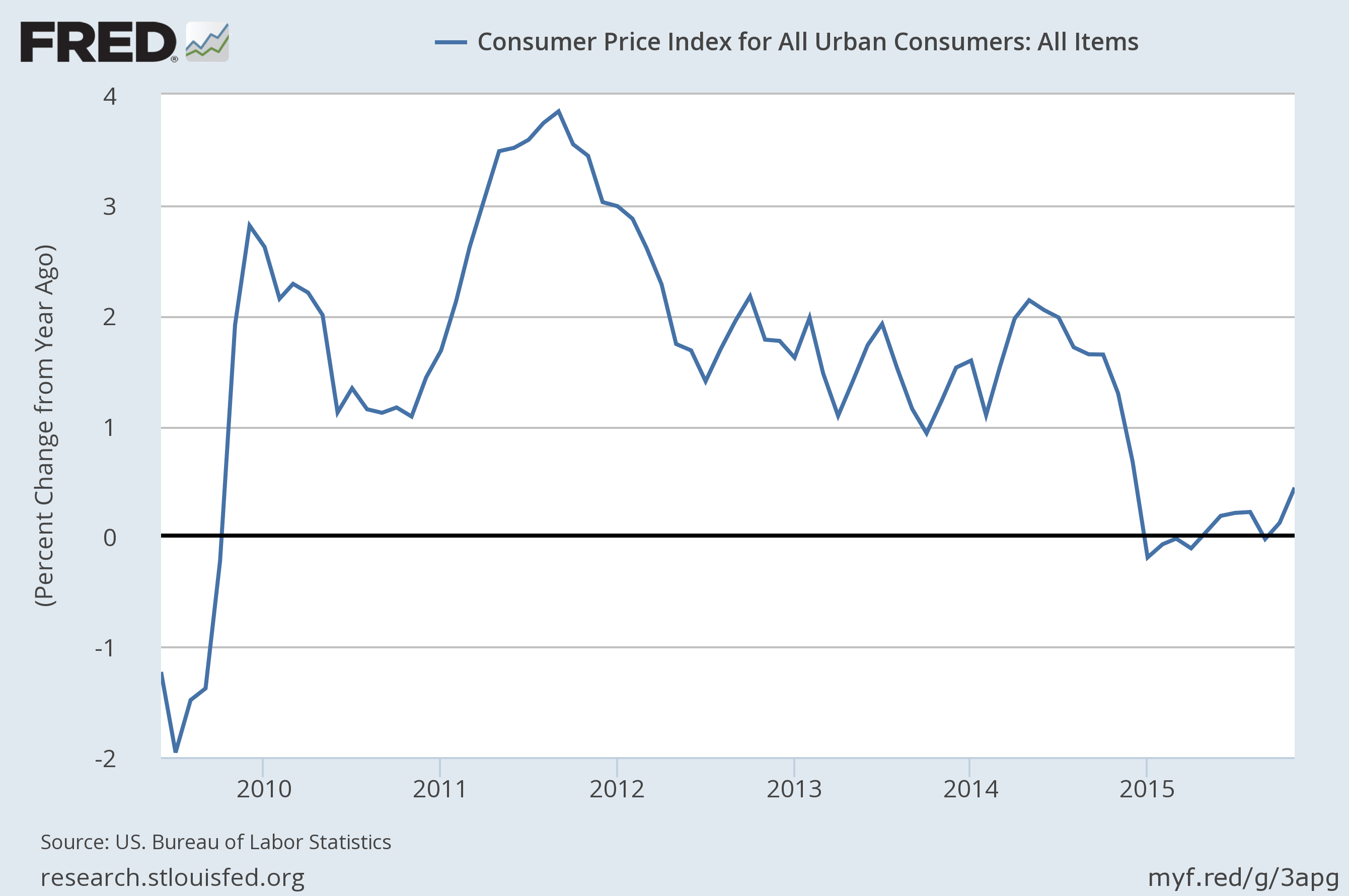

Unfortunately, median household income numbers are published only annually and with a considerable lag (the current data only goes through 2010). In order to try to get a glimpse of recent trends for both total income and labor income versus inflation I offer the following chart.

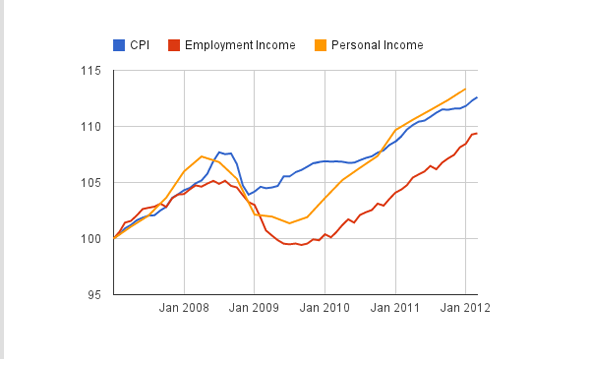

Inflation vs. Employment Income and Personal Income since 2007

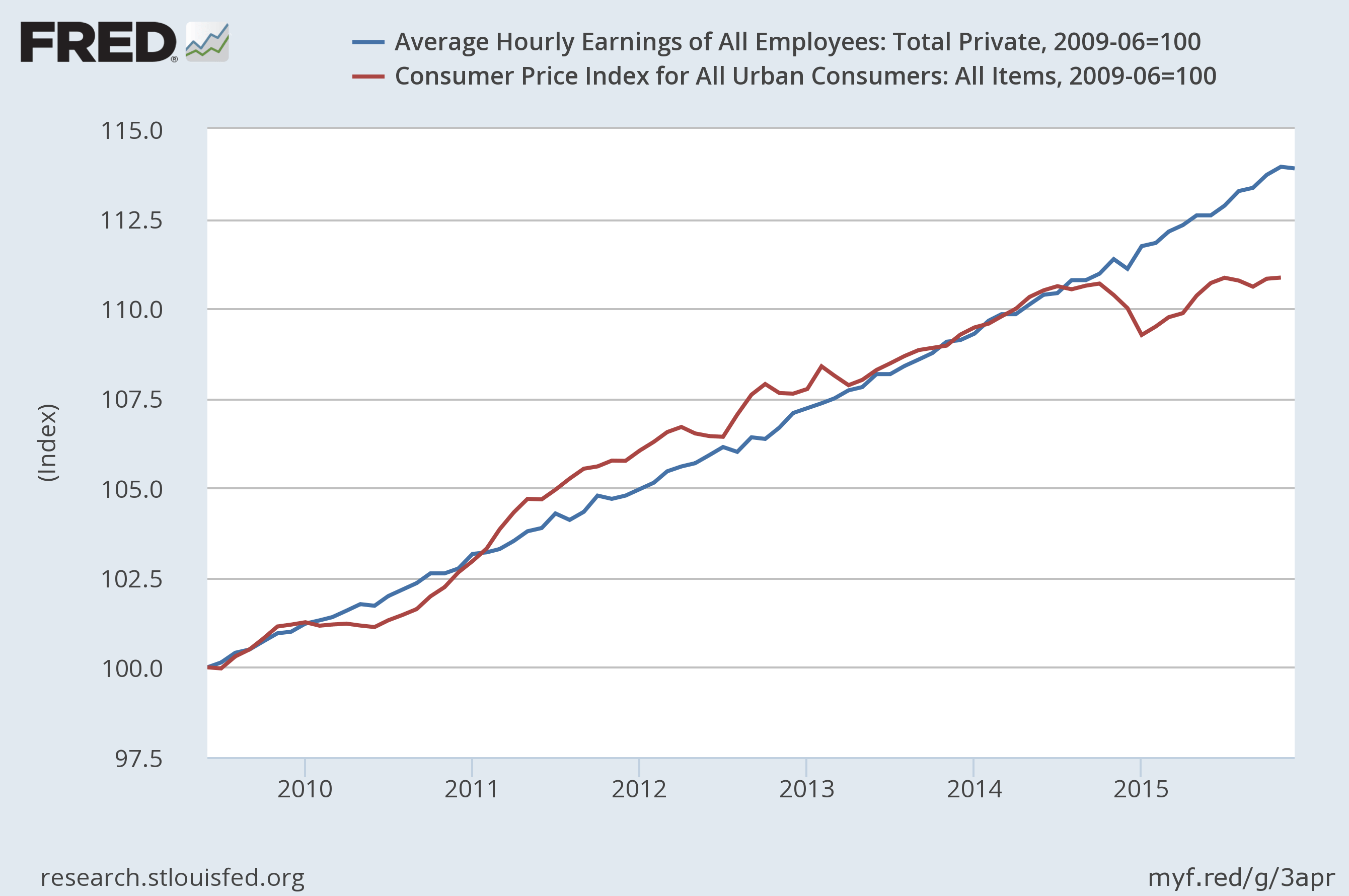

The two income lines on the above chart are in nominal terms and indexed to 100 in January 2007. Along with the two measures of income, I also show consumer price (CPI-U) changes. The first income measure is Personal Income, all income for all persons from all sources — a pretty complete measure I would say. The second measure of income is what I call Total Employment Income. I define that to be (Average Hourly Earnings of All Private Employees) X (Average Weekly Hours of All Private Employees) X (Total Nonfarm Private Payroll Employment). It's my attempt to measure employment income separate from other sources of income. If anyone knows a better or more direct measure, please let me know.

The chart confirms to me what the median household income trends show, that middle income earners have fallen behind relative to inflation because of the recession. While Personal Income has kept up and now exceeds inflation growth since 2007, Total Employment Income still has some distance to make up. In short, I can now make the exceedingly dumb observation that the recession hurt the real income of the average labor force participant.

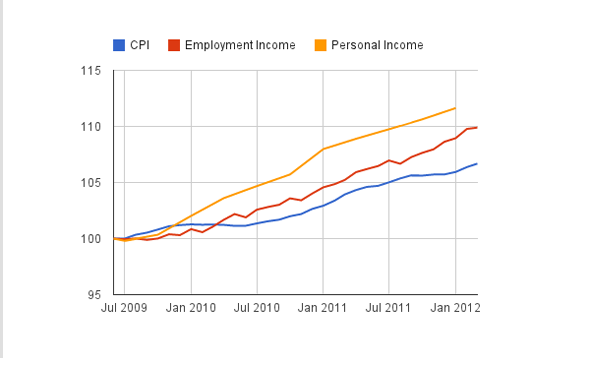

But on a potentially positive note, if you re-index the three series to the technical end of the recession (June 2009), it looks like employment income is doing better than inflation to date (although not as good as Personal Income).

Inflation vs. Employment Income and Personal Income since the end of the Recession

So perhaps the median household income measure for 2011 will reveal the bottom for this cycle was in 2010 and households will gain on real basis when 2011 statistics are released. If that's the case, I won't argue too much with the temporary pursuit of modestly higher inflation. I may not understand all of its mechanisms, but as long as inflation affects wages as well as consumer prices I am comfortable with it.

]]>